A sporting chance – using risk to get ahead of the…

Seeing blind spots, being prepared and taking risk strategically are all key to ensuring an organization can kick goals.

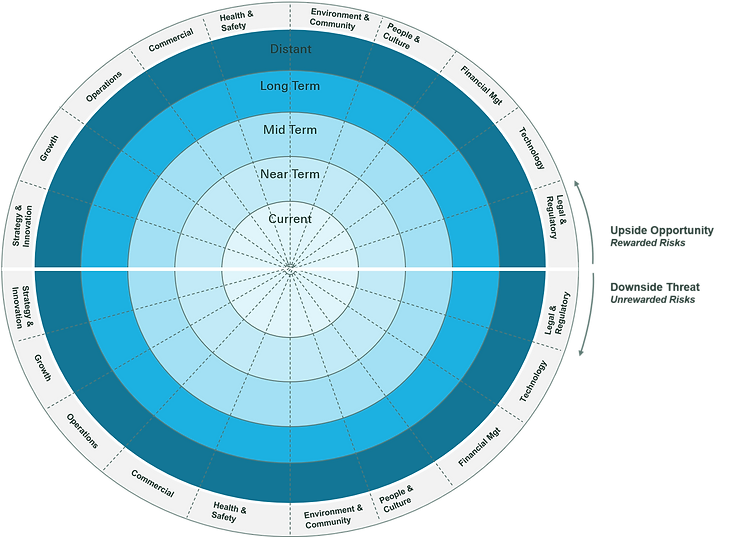

How to see what you don’t see – a practical approach

COVID-19 prompted organisations around the world to ask: what else are we blind to? We run through our risk radar approach.